The debt load of the U.S. is growing at a quicker clip in recent months, increasing about $1 trillion nearly every 100 days.

The nation’s debt permanently crossed over to $34 trillion on Jan. 4, after briefly crossing the mark on Dec. 29, according to data from the U.S. Department of the Treasury. It reached $33 trillion on Sept. 15, 2023, and $32 trillion on June 15, 2023, hitting this accelerated pace. Before that, the $1 trillion move higher from $31 trillion took about eight months.

The national debt eclipsed $34 trillion several years sooner than pre-pandemic projections. The Congressional Budget Office’s January 2020 projections had gross federal debt eclipsing $34 trillion in fiscal year 2029.

But the debt grew faster than expected because of a multi-year pandemic starting in 2020 that shut down much of the U.S. economy. The government borrowed heavily under then President Donald Trump and current President Joe Biden to stabilize the economy and support a recovery. But the rebound came with a surge of inflation that pushed up interest rates and made it more expensive for the government to service its debts.

“So far, Washington has been spending money as if we had unlimited resources,” said Sung Won Sohn, an economics professor at Loyola Marymount University. “But the bottom line is there is no free lunch,” he said, “and I think the outlook is pretty grim.”

The gross debt includes money that the government owes itself, so most policymakers rely on the total debt held by the public in assessing the government’s finances. This lower figure — $26.9 trillion — is roughly equal in size to the U.S. gross domestic product.

Last June, the Congressional Budget Office estimated in its 30-year outlook that publicly held debt will be equal to a record 181% of American economic activity by 2053.

History has shown that there are only three ways out of massive debt – and none of them are pleasant.

Drastically reduce spending by slashing entitlements. By lowering spending below tax collections, it would free up cash flow to service the debt while stopping adding to the debt. The result will be mass riots by all of the people getting cut off and general societal instability.

Print money like crazy to pay the debt. This will crash the currency and spin into hyperinflation. Again… mass riots, instability, nation falls.

Default on the debt. Once again, it would crash the economy… mass riots, instability, nation falls.

#1 is the best option, but it takes political courage. That is severely lacking in America.

WASHINGTON (AP) — The nation’s gross national debt has surpassed $31 trillion, according to a U.S. Treasury report released Tuesday that logs America’s daily finances.

Edging closer to the statutory ceiling of roughly $31.4 trillion — an artificial cap Congress placed on the U.S. government’s ability to borrow — the debt numbers hit an already tenuous economy facing high inflation, rising interest rates and a strong U.S. dollar.

[…]

The Congressional Budget Office earlier this year released a report on America’s debt load, warning in its 30-year outlook that, if unaddressed, the debt will soon spiral upward to new highs that could ultimately imperil the U.S. economy.

The federal deficit surpassed $1 trillion in the first 11 months of fiscal 2019, the Congressional Budget Office (CBO) said Monday.

The deficit presently stands at $1.068 trillion, though it is likely to be reduced in September as quarterly tax payments are paid.

“In its most recent baseline projections, CBO estimated that the 2019 budget deficit would be $960 billion,” the CBO noted. That amount would be $181 billion higher than last year’s deficit.

The deficit as of Monday was running $168 billion ahead of the deficit in the last fiscal year at this time.

While mandatory spending such as Social Security and Medicare drive the deficit, it has shot up under President Trump‘s watch following the GOP tax cut bill and a series of bipartisan agreements to raise spending on both defense and domestic priorities.

The CBO has called the nation’s fiscal path “unsustainable,” noting that payments on interest alone were on track to overtake both defense and domestic spending by 2046.

We have seen this scenario play out time and time again in countries all over the world. At some point, the debt becomes so overwhelming that there are only three choices:

Massive cuts in spending to free up money to pay debt that results in civil unrest. It would be better to cut smaller now than just abruptly abandon things like Social Security in the future.

Cancel the debt and leave all of the bond holders empty handed. This would destroy our nation’s ability to borrow while wiping out the wealth of millions of people.

Print more money to pay the debt. The result is rampant inflation that wipes out the wealth and swamps the incomes of every American. This is the option most often chosen by politicians because it’s easier.

There is no good outcome to this kind of debt. It’s a nation killer.

WASHINGTON (AP) — The national debt has passed a new milestone, topping $22 trillion for the first time.

The Treasury Department’s daily statement showed Tuesay that total outstanding public debt stands at $22.01 trillion. It stood at $19.95 trillion when President Donald Trump took office on Jan. 20, 2017.

The debt figure has been rising at a faster pace following passage of Trump’s $1.5 trillion tax cut in December 2017 and action by Congress last year to increase spending on domestic and military programs.

My column for the West Bend Daily News is online. It was one of those that I started out writing with one intent and it turned into something completely different. That happens sometimes. Here it is:

We are a little less than seven weeks away from when the first votes will be cast to choose President Barack Obama’s successor. While the presidential election season has been entertaining so far, it is time for Americans to begin to seriously assess the candidates and the country we will elect one of them to lead. Our nation has some grim challenges ahead that will need to be addressed with honesty, intelligence and resoluteness.

It has fallen out of favor to discuss in polite circles, but America has a debt problem. Much like many American citizens have too much credit card or student loan debt, the nation has a debt problem that cannot be ignored.

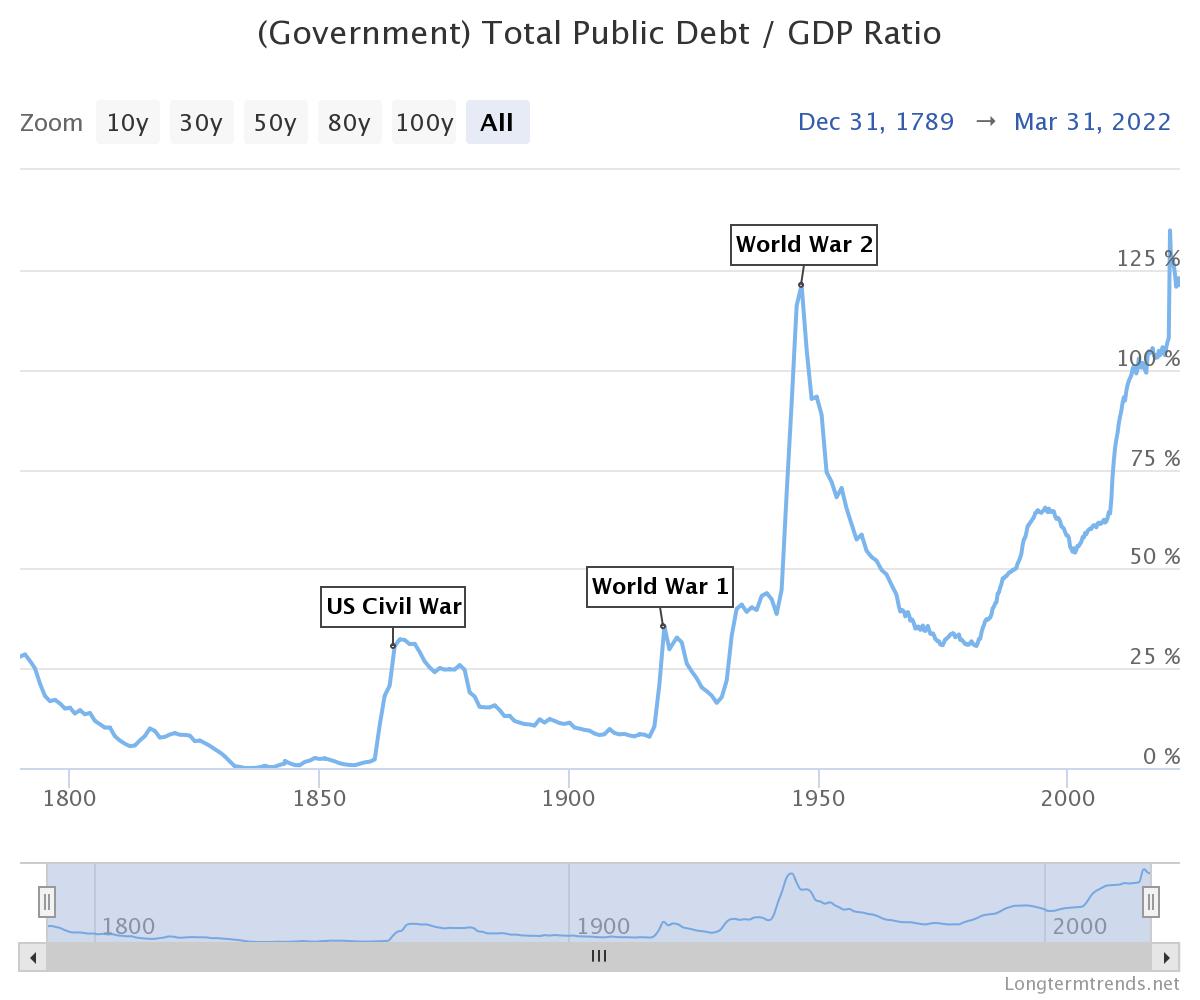

About this time three years ago, America’s national debt exceeded the gross domestic product of the nation, and has continued to rise. That means that if every good and service that the entire American economy produced in a single year was to be put toward retiring our nation’s debt, we would still not pay it all off. America has not had this much debt since the entirety of our nation’s resources were marshaled to fight World War II.

What is driving the debt is very simple: Our federal government is spending far more money than it takes in. Where does the money go? The majority of federal spending goes to healthcare, Social Security and other entitlements (only about 20 percent goes to our active military and veterans). Under Obama, our nation took on more debt than every other president combined. Essentially, our nation is borrowing money that our children and grandchildren will have to pay back to pay the retirement and healthcare costs of people living today. It is a generational transfer of wealth.

Unfortunately, the official national debt, which is money our nation has borrowed to pay our bills, is not the entirety of what our nation owes. The almost $19 trillion dollar national debt does not include future monies that our nation has promised to pay. If you add in those obligations, American taxpayers are on the hook for more than $127 trillion, according to Forbes. Some estimates put that number even higher. As it stands now, there is no way to keep those promises. There simply is not enough money.

There are only two ways for a nation to pay off debt. The first way is to spend less than it collects in taxes. If the government takes in more taxes than it spends, it can gradually pay off the debt over time. This has only happened briefly in most of our lifetimes, from 1998 through 2001. Other than those few periods, neither Republicans nor Democrats have shown an ability to control spending since President Dwight Eisenhower. And while the federal government could raise taxes (again), it still could not raise them enough to match the current spending without sending the national economy into a depression. The mantra to just “tax the rich” is a child’s answer to an adult problem.

The second way a nation can pay off its debt is to print money. Unlike individual families or states, a nation controls the currency and can print its own money. But every action has a reaction. As the treasury floods the economy with new money to pay off old debts, it devalues the currency and makes everything more expensive for average Americans whose wages rarely keep up in an era of high inflation. Also, the people taking on America’s debt are less willing to take on debt that will be paid back with devalued currency, so they either insist on an everincreasing interest rate or refuse to take on the debt at all.

The federal debt is just one challenge that the next president will face. He or she will also have to confront the onslaught of violent radical Islamists currently being championed by the Islamic State; a sluggish national economy that has been treading water for years; the rise of China and Russia; a nuclear Iran; the problems created by our current open borders; and many other problems that affect the way Americans’ live their lives.

The cage match of the presidential election has been fun to watch so far, but the time for silliness and silly candidates is over. Now it is time to think seriously about choosing the leader of the free world.